①In 2025, the integration of small and medium-sized financial institutions across regions achieved significant results, with the number of legal entities of banking financial institutions decreasing by 225 compared to the end of 2024, and by 534 compared to the end of the '13th Five-Year Plan'. ②State-owned large commercial banks participated in the risk resolution and asset integration of rural commercial banks, further accelerating the clearance of local small and medium-sized banks.

Cailian Press reported on February 5 (edited by Yang Bin) that after the start of the year, there were frequent moves in the reform of local financial institutions, with multiple provinces announcing the progress of preparations for provincial rural commercial banks. In recent years, the 'reduction in quantity and improvement in quality' of small and medium-sized banks has accelerated. Data shows that by the end of 2025, the number of banking financial institutions decreased by 534 compared to the end of the '13th Five-Year Plan', with 225 banks 'disappearing' that year.

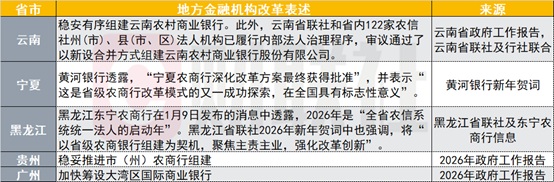

Yunnan was the first province in 2026 to clearly outline the implementation path for the reform of the provincial credit union. According to the recent government work report of Yunnan Province and the joint announcement by the provincial credit union and the provincial rural credit cooperatives, Yunnan is steadily and orderly forming Yunnan Rural Commercial Bank. The internal corporate governance procedures have been fully carried out by the provincial credit union and 122 rural credit cooperatives at the prefecture (city) and county (city, district) levels, approving the relevant resolutions to establish Yunnan Rural Commercial Bank Co., Ltd. through a new merger.

Ningxia Yellow River Rural Commercial Bank disclosed in its New Year's message in 2026 that the reform plan for Ningxia Rural Commercial Bank had finally been approved. It is reported that Ningxia will use Yellow River Bank as the main body to promote the absorption and merger of the remaining 19 rural credit institutions within its jurisdiction, ultimately forming a 'single legal entity bank' pattern for the entire province. Heilongjiang also designated 2026 as the starting year for the reform of a unified legal entity system in the rural credit system, officially putting the establishment of a provincial rural commercial bank on the agenda.

Ningxia Yellow River Rural Commercial Bank disclosed in its New Year's message in 2026 that the reform plan for Ningxia Rural Commercial Bank had finally been approved. It is reported that Ningxia will use Yellow River Bank as the main body to promote the absorption and merger of the remaining 19 rural credit institutions within its jurisdiction, ultimately forming a 'single legal entity bank' pattern for the entire province. Heilongjiang also designated 2026 as the starting year for the reform of a unified legal entity system in the rural credit system, officially putting the establishment of a provincial rural commercial bank on the agenda.

Guizhou proposed to steadily advance the formation of municipal (prefecture) rural commercial banks. Previously, Guizhou completed the restructuring of the provincial credit union, establishing Guizhou Rural Commercial Joint Bank in December 2025. With the establishment of municipal and prefectural rural commercial banks, Guizhou will form the prototype of a new two-tier legal entity structure consisting of 'provincial rural commercial joint bank + municipal and prefectural rural commercial banks'.

Figure: Statements from local authorities regarding financial institution reforms after the start of the year

(Data Source: Enterprise Early Warning, compiled by Cailian News)

In recent years, the 'reduction in quantity and improvement in quality' of small and medium-sized banks has been a key focus of the reform of local financial institutions. The Central Economic Work Conference in 2025 once again emphasized 'deeply promoting the reduction in quantity and improvement in quality of small and medium-sized financial institutions, and continuously deepening comprehensive reforms in capital market investment and financing.' In recent years, the Central Document No. 1 has also included statements about 'accelerating the reform of rural credit cooperatives.'

According to statistics from Yan Ziqi, Chief Fixed Income Analyst at Guohai Securities, the integration of small and medium-sized financial institutions across regions achieved significant results in 2025, with the number of legal entities of banking financial institutions decreasing by 225 compared to the end of 2024, and by 534 compared to the end of the '13th Five-Year Plan.' During the integration process, city commercial banks mainly adopted the model of absorption and merger to participate in the integration of rural banks within their jurisdictions; rural commercial banks followed the reform of the rural credit system, promoting the establishment of provincial rural commercial banks under four models: 'unified legal entity,' 'joint bank,' 'financial services company,' and 'financial holding company.'

According to publicly available information compiled by Cailian Press, at least 13 provinces have implemented provincial rural commercial bank reforms in recent years, including Zhejiang Rural Commercial Joint Bank, Liaoning Rural Commercial Bank, Shanxi Rural Commercial Joint Bank, Sichuan Rural Commercial Joint Bank, Guangxi Rural Commercial Joint Bank, Hainan Rural Commercial Bank, Henan Rural Commercial Bank, Jiangxi Rural Commercial Joint Bank, and Inner Mongolia Rural Commercial Bank. In 2025, seven provinces implemented upgraded rural commercial bank reforms; in the second half of the year, Jilin Rural Commercial Bank, Xinjiang Rural Commercial Bank, and Guizhou Rural Commercial Joint Bank were successively established.

Additionally, state-owned large commercial banks participated in the risk resolution and asset integration of rural commercial banks. ICBC, Bank of Communications, and Agricultural Bank of China promoted the 'village-to-branch' initiative in 2025, further accelerating the clearance of local small and medium-sized banks.

The United Credit Ratings Research believes that the ongoing reforms of provincial credit cooperatives, the mergers and reorganizations of rural financial institutions, and the absorption and integration of village and township banks into branch offices as part of the restructuring efforts for small and medium-sized banks in China have, on one hand, further standardized and optimized the corporate governance systems of rural financial institutions. On the other hand, these measures have also facilitated the integration and optimization of financial resources, thereby enhancing competitiveness and risk resistance capabilities.